Application: Optimal Growth#

![]()

Exercises from the Class Notes#

Exercise 3.1#

Assume that (A1)-(A3) hold. Which of the assumptions presented in Lectures 1 and 2 are satisfied?

Solution

Assumptions A1.1, A1.2, A2.1, A2.3, and A2.4. In assumption A2.2, \(F\) is not bounded under (A1)-(A3). However, we can assume that capital is at most equal to the maximum maintainable capital stock.

Exercise 3.2#

Show that, for any \(k_0 \in (0,k_{max}]\), the optimal sequence \(\{k_t\}_{t=0}^{\infty}\) defined by \(k_{t+1}=g(k_t)\) converges to \(k^*=f'^{-1}(1/\beta)\).

Solution

From fact that \(v\) is strictly concave, we have

with equality iff \(g\left(k\right) = k\). By the FOC and EC conditions and use the fact that \(U^{'}\left(c\right)>0\), we can conclude that

with equality iff \(g\left(k\right) = k\). Since \(f\) is concave, it follows that \(f^{'}\left(k\right) \stackrel{>}{<} \frac{1}{\beta}\) as \(k\stackrel{<}{>} k^{*}\) and \(k \stackrel{>}{<} g\left(k\right)\) that as \(k \stackrel{>}{<} k^{*}\).

Consider the optimal sequence \(\{k_t\}_{t=0}^{\infty}\) defined by \(k_{t+1}=g(k_t)\). If \(k_{t} \geq k^{*}\), then \(k_{t+1} =g(k_t)\leq k_{t}\) decreases until \(k = k^{*}\). Likewise, if \(k_{t} \leq k^{*}\), then \(k_{t+1}=g(k_t) \geq k_{t}\) increases until \(k = k^{*}\). Therefore the optimal sequence \(\{k_t\}_{t=0}^{\infty}\) converges to \(k^{*}\).

Exercise 3.3#

Write a code in Python that uses an iterative procedure to solve for the value function of the optimal growth model.

Solution

# -*- coding: utf-8 -*-

"""

Created on Sun Nov 18 14:37:30 2018

@author: Bruno

"""

#==============================================================================

# Recursive Methods - Optimal Growth

#==============================================================================

import os

import numpy as np

from scipy.optimize import fminbound

def bellman_operator(w, grid, β, u, f, Tw=None, compute_policy=0):

# === Apply linear interpolation to w === #

w_func = lambda x: np.interp(x, grid, w)

# == Initialize Tw if necessary == #

if Tw is None:

Tw = np.empty_like(w)

if compute_policy:

σ = np.empty_like(w)

# == set Tw[i] = max_c { u(c) + β E w(f(y - c) z)} == #

for i, y in enumerate(grid):

def objective(c, y=y):

# return #Your code goes here

return - u(c) - β * w_func(f(y - c))

c_star = fminbound(objective, 1e-10, y)

if compute_policy:

# σ[i] = #Your code goes here #y_(t+1) as a function of y_t

σ[i] = f(y-c_star) #y_(t+1) as a function of y_t

# Tw[i] = #Your code goes here

Tw[i] = - objective(c_star)

if compute_policy:

return Tw, σ

else:

return Tw

def solve_optgrowth(initial_w, grid, β, u, f, tol=1e-4, max_iter=500):

w = initial_w # Set initial condition

error = tol + 1

i = 0

# == Create storage array for bellman_operator. Reduces memory

# allocation and speeds code up == #

Tw = np.empty(len(grid))

# Iterate to find solution

while error > tol and i < max_iter:

w_new = bellman_operator(w,

grid,

β,

u,

f,

Tw)

# error = #Your code goes here

error = np.max(np.abs(w_new - w))

w[:] = w_new

i += 1

print("Iteration "+str(i)+'\n Error is '+str(error)+'\n') if i % 50 == 0 or error < tol else None

# Computes policy

policy = bellman_operator(w,

grid,

β,

u,

f,

Tw,

compute_policy=1)[1]

return [w, policy]

class CES_OG:

"""

Constant elasticity of substitution optimal growth model so that

y = f(k) = k^α

The class holds parameters and true value and policy functions.

"""

def __init__(self, α=0.4, β=0.96, sigma=0.9):

self.α, self.β, self.sigma = α, β, sigma

def u(self, c):

" Utility "

return (c**(1-self.sigma)-1)/(1-self.sigma)

def f(self, k):

" Deterministic part of production function. "

return k**self.α

# Creation of the model

ces = CES_OG()

# == Unpack parameters / functions for convenience == #

α, β, sigma = ces.α, ces.β, ces.sigma

### Setup of the grid

grid_max = 1 # Largest grid point

grid_size = 200 # Number of grid points

grid = np.linspace(1e-5, grid_max, grid_size)

# Initial conditions and shocks

initial_w = 5 * np.log(grid)

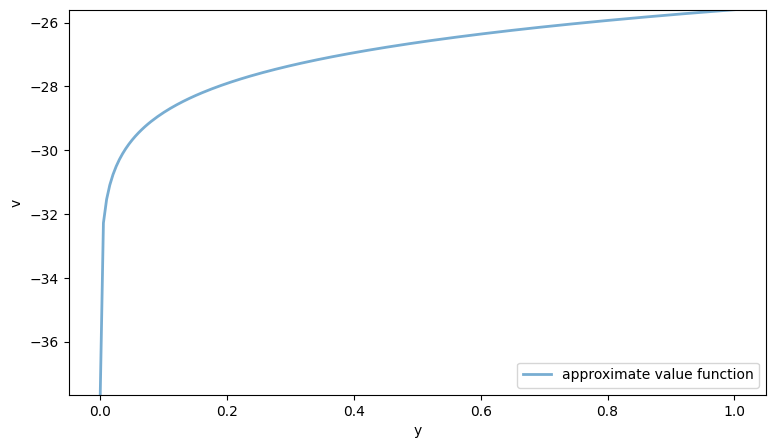

# Computation of the value function

solve = solve_optgrowth(initial_w, grid, β, u=ces.u,

f=ces.f, tol=1e-4, max_iter=500)

value_approx = solve[0]

policy_function = solve[1]

Iteration 50

Error is 0.13013875164658728

Iteration 100

Error is 0.016903175250330804

Iteration 150

Error is 0.002195482297175033

Iteration 200

Error is 0.0002851634526557234

Iteration 226

Error is 9.866159687632603e-05

#==============================================================================

# Plotting value function

#==============================================================================

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(9, 5))

ax.set_ylim(min(value_approx), max(value_approx))

ax.plot(grid, value_approx, lw=2, alpha=0.6, label='approximate value function')

ax.set_xlabel('y')

ax.set_ylabel('v')

ax.legend(loc='lower right')

plt.show()

#==============================================================================

# Plotting Policy function

#==============================================================================

fig, ax = plt.subplots(figsize=(9, 5))

ax.set_ylim(min(policy_function), max(policy_function))

ax.plot(grid, policy_function, lw=2, alpha=0.6, label='approximate policy function')

# 45° line

ax.plot(grid, grid, lw=2, alpha=0.6, label='45 degrees line')

ax.set_xlabel('y_t')

ax.set_ylabel('y_(t+1)')

ax.legend(loc='lower right')

plt.show()

Additional Exercises#

Exercise 3.4 (Sufficiency of Euler and transversality conditions)#

Assume that the Assumptions in Lecture 2 are satisfied.

Show that the sequence \(\{x^*_{t+1}\}_{t=0}^{\infty}\) with \(x^*_{t+1}\in\Gamma(x_t)\) for all \(t\geq 0\), is optimal for the Sequential Problem if it satisfies the Euler equation and the following transversality condition: \(\lim_{t\rightarrow \infty} \beta^t F_1(x^*_{t},x^*_{t+1})\cdot x^*_{t}=0\).

Can we replace the transversality condition in 1 with that of the recursive problem: \(\lim_{t\rightarrow \infty} \beta^t V(x^*_{t})=0\)?

Solution

It is sufficient to show that the difference between the objective function in the sequential problem evaluated at \(\{x^{*}\}\) and at \(\{x_{t}\}\) is nonnegative.

Since \(F\) is continuous, concave, and differentiable,

Since \(x_{0}^{*} - x_{0} = 0\), rearranging terms givees

Since \(\{x^{*}\}\) satisfies the FOC, the terms in the summation are all zero. Therefore, by the FOC and using the Euler Equation to substitute the last remaining term, we obtain

It then follows that \(D\geq 0\), establishing the desired result.

Yes, because the value function is concave in this setting.

Exercise 3.5#

Let \(\bar{k}=f(\bar{k})\) denote the maximum maintainable capital stock. Show that the standard assumptions on \(f\) and \(U\) ensure that for any \(k\in(0,\bar{k}]\), the solution of the Bellman equation is at an interior value for \(k'\), so that \(v\) is continuously differentiable on \((0,\bar{k}]\), and that the FOC and Envelope Condition (EC) hold for all \(k\in(0,\bar{k}]\).

Use the EC to show that the policy function \(g(k)\) is strictly increasing.

Solution

Pick any \(k\in (0,\overline{k}]\). To see that \(g\left(k\right) \in \left(0,\overline{k}\right)\), suppose \(g\left(k\right) = 0\). Then,

but the left-hand side is finite while the right-had side is not. There \(k\left(k\right) = 0\) cannot not be optimal.

Suppose then \(g\left(k\right) = \overline{k}\). Because \(k\in (0,\overline{k}]\), and consumption is nonnegative, it must be that \(k = \overline{k}\). Hence,

but the left-hand side of the inequality stated above is not finite. On the other hand, feasibility requires that \(g\left(\overline{k}\right)\leq \overline{k}\). If \(g\left(\overline{k}\right)= \overline{k}\), this implies zero consumption even after, which is suboptimal. Hence \(g\left(\overline{k}\right)< \overline{k}\). But

and the right-hand side is finite, which is a contradiction. Therefore, the solution of the Bellman equation is an interior value for \(k^{'}\). By Theorem 4.11 (Differentiability of the value function), v is contiunously differentiable on \((0,\overline{k}]\).

Pick \(k,\ k^{'}\in (0,\overline{k}]\), with \(k<k^{'}\). Suppose \(g\left(k\right)\geq g\left(k^{'}\right)\). Then \(v\) being strictly concave implies

Hence, by \(U\) being strictly concave,

Then, \(f\) being strictily increasing implies

and so \(g\left(k^{'}\right)>g\left(k\right)\), which is a contraction.

Exercise 3.6#

Consider a modification of the canonical growth model where capital goods are produced using only labor. We endow the consumer with one unit labor, and assume that \(c_t=n_tf(k_t/n_t) \text{ and } k_{t+1}=1-n_t.\) We also assume that \(\lim_{n\rightarrow 0} nf(k,n)=0\) for all \(k\in[0,1]\).

Write the Bellman equation. Derive the FOC and EC.

Find a necessary condition that must be satisfied by the stationary capital stock. Prove that it indeed identifies the steady-state.

Let \(U(c)=c^{\alpha}\) with \(\alpha \in (0,1)\) and \(f(x)=x^{\theta}\) with \(\theta \in (0,1)\). Use the FOC to show that the policy function \(g(k)\) is strictly decreasing on \([0,1]\).

Solution

The Bellman equation can be written as

Let \(g\) denote the policy funtion. The first-order and envelope conditions are given by

Setting \(g\left(k_{t}\right) = k_{t}\) and eliminating \(k_{t}^{'}\), a necessary condition for a stationary point is

By the assumptions on \(f\), the equation above has exactly one solution, denoted as \(k^{*}\). Since \(v\) is strictly concave, the condition in Exercise 3.2 holds. Substituting from the FOC and EC, we have

with equality only if \(g\left(k_{t}\right) = k_{t}\). Therefore \(k^{*}\) is indeed a stationary point.

Pick \(k,\ k^{'}\in (0,\overline{k}]\), with \(k<k^{'}\). Suppose \(g\left(k\right)\geq g\left(k^{'}\right)\). With the specific function forms, the FOC is given by

As \(v\) is strictly concave, we have

which implies

where

Hence,

and so \(g\left(k^{'}\right)<g\left(k\right)\), which is a contradiction.

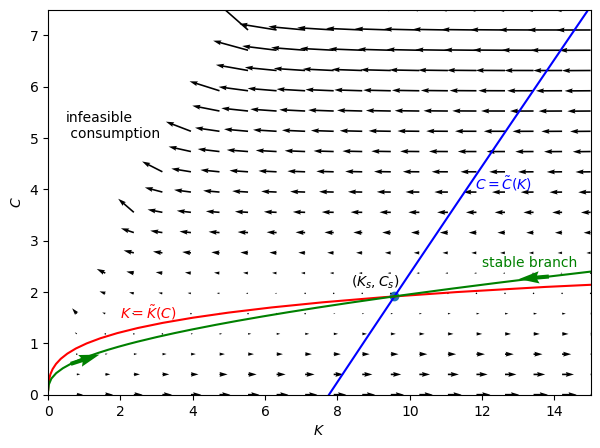

Phase Diagram#

The code below is borrowed from QuantEcon

It displays the phase diagram of the infinite horizon growth model when

Utility function is CRRA: \(U(c)=\frac{c^{1-\gamma}}{1-\gamma}\);

Production function is Cobb-Douglas with fixed labor supply: \(F(K,1)=K^{\alpha}\).

import matplotlib.pyplot as plt

from numba import njit, float64

from numba.experimental import jitclass

import numpy as np

from quantecon.optimize import brentq

We first define a jitclass that stores parameters and functions that define our economy.

planning_data = [

('γ', float64), # Coefficient of relative risk aversion

('β', float64), # Discount factor

('δ', float64), # Depreciation rate on capital

('α', float64), # Return to capital per capita

('A', float64) # Technology

]

@jitclass(planning_data)

class PlanningProblem():

def __init__(self, γ=2, β=0.95, δ=0.02, α=0.33, A=1):

self.γ, self.β = γ, β

self.δ, self.α, self.A = δ, α, A

def u(self, c):

'''

Utility function

ASIDE: If you have a utility function that is hard to solve by hand

you can use automatic or symbolic differentiation

See https://github.com/HIPS/autograd

'''

γ = self.γ

return c ** (1 - γ) / (1 - γ) if γ!= 1 else np.log(c)

def u_prime(self, c):

'Derivative of utility'

γ = self.γ

return c ** (-γ)

def u_prime_inv(self, c):

'Inverse of derivative of utility'

γ = self.γ

return c ** (-1 / γ)

def f(self, k):

'Production function'

α, A = self.α, self.A

return A * k ** α

def f_prime(self, k):

'Derivative of production function'

α, A = self.α, self.A

return α * A * k ** (α - 1)

def f_prime_inv(self, k):

'Inverse of derivative of production function'

α, A = self.α, self.A

return (k / (A * α)) ** (1 / (α - 1))

def next_k_c(self, k, c):

''''

Given the current capital Kt and an arbitrary feasible

consumption choice Ct, computes Kt+1 by state transition law

and optimal Ct+1 by Euler equation.

'''

β, δ = self.β, self.δ

u_prime, u_prime_inv = self.u_prime, self.u_prime_inv

f, f_prime = self.f, self.f_prime

k_next = f(k) + (1 - δ) * k - c

c_next = u_prime_inv(u_prime(c) / (β * (f_prime(k_next) + (1 - δ))))

return k_next, c_next

# Create economy instance

pp = PlanningProblem()

# Compute stable manifold for Consumption

@njit

def C_tilde(K, pp):

return pp.f(K) + (1 - pp.δ) * K - pp.f_prime_inv(1 / pp.β - 1 + pp.δ)

# Compute stable manifold for Capital

@njit

def K_diff(K, C, pp):

return pp.f(K) - pp.δ * K - C

@njit

def K_tilde(C, pp):

res = brentq(K_diff, 1e-6, 100, args=(C, pp))

return res.root

# Compute steady-state by combining the two stable manifolds

@njit

def K_tilde_diff(K, pp):

K_out = K_tilde(C_tilde(K, pp), pp)

return K - K_out

res = brentq(K_tilde_diff, 8, 10, args=(pp,))

Ks = res.root

Cs = C_tilde(Ks, pp)

Ks, Cs

# Implements the shooting algorithm for the planning problem.

@njit

def shooting(pp, c0, k0, T=10):

'''

Given the initial condition of capital k0 and an initial guess

of consumption c0, computes the whole paths of c and k

using the state transition law and Euler equation for T periods.

'''

if c0 > pp.f(k0) + (1 - pp.δ) * k0:

print("initial consumption is not feasible")

return None

# initialize vectors of c and k

c_vec = np.empty(T+1)

k_vec = np.empty(T+2)

c_vec[0] = c0

k_vec[0] = k0

for t in range(T):

k_vec[t+1], c_vec[t+1] = pp.next_k_c(k_vec[t], c_vec[t])

k_vec[T+1] = pp.f(k_vec[T]) + (1 - pp.δ) * k_vec[T] - c_vec[T]

return c_vec, k_vec

# Use a bisection method to match the terminal condition

@njit

def bisection(pp, c0, k0, T=10, tol=1e-4, max_iter=500, k_ter=0, verbose=True):

# initial boundaries for guess c0

c0_upper = pp.f(k0)

c0_lower = 0

i = 0

while True:

c_vec, k_vec = shooting(pp, c0, k0, T)

error = k_vec[-1] - k_ter

# check if the terminal condition is satisfied

if np.abs(error) < tol:

if verbose:

print('Converged successfully on iteration ', i+1)

return c_vec, k_vec

i += 1

if i == max_iter:

if verbose:

print('Convergence failed.')

return c_vec, k_vec

# if iteration continues, updates boundaries and guess of c0

if error > 0:

c0_lower = c0

else:

c0_upper = c0

c0 = (c0_lower + c0_upper) / 2

We now compute two trajectories towards the steady-state that start from different sides of K_{S}.

c_vec1, k_vec1 = bisection(pp, 5, 15, T=200, k_ter=Ks)

c_vec2, k_vec2 = bisection(pp, 1e-3, 1e-3, T=200, k_ter=Ks)

# Plot Phase Diagram

fig, ax = plt.subplots(figsize=(7, 5))

K_range = np.arange(1e-1, 15, 0.1)

C_range = np.arange(1e-1, 2.3, 0.1)

# C tilde

ax.plot(K_range, [C_tilde(Ks, pp) for Ks in K_range], color='b')

ax.text(11.8, 4, r'$C=\tilde{C}(K)$', color='b')

# K tilde

ax.plot([K_tilde(Cs, pp) for Cs in C_range], C_range, color='r')

ax.text(2, 1.5, r'$K=\tilde{K}(C)$', color='r')

# stable branch

ax.plot(k_vec1[:-1], c_vec1, color='g')

ax.plot(k_vec2[:-1], c_vec2, color='g')

ax.quiver(k_vec1[5], c_vec1[5],

k_vec1[6]-k_vec1[5], c_vec1[6]-c_vec1[5],

color='g')

ax.quiver(k_vec2[5], c_vec2[5],

k_vec2[6]-k_vec2[5], c_vec2[6]-c_vec2[5],

color='g')

ax.text(12, 2.5, r'stable branch', color='g')

# (Ks, Cs)

ax.scatter(Ks, Cs)

ax.text(Ks-1.2, Cs+0.2, '$(K_s, C_s)$')

# arrows

K_range = np.linspace(1e-3, 15, 20)

C_range = np.linspace(1e-3, 7.5, 20)

K_mesh, C_mesh = np.meshgrid(K_range, C_range)

next_K, next_C = pp.next_k_c(K_mesh, C_mesh)

ax.quiver(K_range, C_range, next_K-K_mesh, next_C-C_mesh)

# infeasible consumption area

ax.text(0.5, 5, "infeasible\n consumption")

ax.set_ylim([0, 7.5])

ax.set_xlim([0, 15])

ax.set_xlabel('$K$')

ax.set_ylabel('$C$')

plt.show()