Reinforcement Learning#

Multi-Armed Bandits#

Acknowledgement: This presentation is borrowed from Tim Miller’s website Mastering Reinforcement Learning.

Definition#

A multi-armed bandit is defined by a set of random variables \(X_{i,k}\) where: (i) \(i\in\{1,2,..,N\}\) is the arm of the bandit; (ii) \(k\) is the index of the play.

Draws are independently distributed and the gambler does not know the probability distributions of the random variables. The gambler plays succesive rounds, observes the reward from the selected arm after each round, and then adjusts her strategy with the objective of maximizing the rewards collected over all rounds.

Q-Value#

The Q-value of an action is defined as the expected reward for taking action \(a\), i.e. \(Q(a) = \mathbb{E}[R | A = a]\). The true Q-value being unknown, it must be estimated. In practice, one can use the sample average of observed rewards to estimate the Q-value:

where \(t\) is the number of rounds so far, \(N(a)\) is the number of times action \(a\) has been selected in previous rounds, and \(X_{\{a,i\}}\) is the reward obtained in the \(i-th\) round for playing arm \(a\).

Exploration-Exploitation Dilemna#

After having explored her options for some time, the grambler forms a belief for the Q-value of each arm. Then she can switch to a greedy strategy, selecting only the actions that have given her the best rewards so far. However, being greedy may also lead the gambler to overlook the most profitable arm. Thus, she should follow a strategy that exploit the actions that have been profitable so far, while still exploring other actions. This tension is known as the exploration vs. exploitation dilemma.

Implementation#

We borrowed the code from Tim Miller’s website Mastering Reinforcement Learning. A smaller repo containing all the programs required for this implementation is available HERE.

The implementation of the strategy below inherits from the class MultiArmedBandit:

class MultiArmedBandit():

""" Select an action for this state given from a list given a Q-function """

def select(self, state, actions, qfunction):

abstract

""" Reset a multi-armed bandit to its initial configuration """

def reset(self):

self.__init__()

Simulation#

To demonstrate the effect of a multi-armed bandit strategy, we use the simulation below. The simulation is an implementation of a simple multi-armed bandit problem with five actions and their associated probabilities.

The simulation runs 2000 episodes of a bandit problem, with each episode being 1000 steps long. At each step, the agent must chose an action. At the beginning of each episode, the bandit strategies are reset. The simulation returns a list of lists, representing the reward received at each step of each episode. The aim for the bandit is to maximise the expected rewards over each episode.

from collections import defaultdict

import random

from qtable import QTable

""" Run a bandit algorithm for a number of episodes, with each episode

being a set length.

"""

def run_bandit(bandit, episodes=200, episode_length=500, drift=True):

# The actions available

actions = [0, 1, 2, 3, 4]

# A dummy state

state = 1

rewards = []

for _ in range(0, episodes):

bandit.reset()

# The probability of receiving a payoff of 1 for each action

probabilities = [0.1, 0.3, 0.7, 0.2, 0.1]

# The number of times each arm has been selected

times_selected = defaultdict(lambda: 0)

qtable = QTable()

episode_rewards = []

for step in range(0, episode_length):

# Halfway through the episode, change the probabilities

if drift and step == episode_length / 2:

probabilities = [0.5, 0.2, 0.0, 0.3, 0.3]

# Select an action using the bandit

action = bandit.select(state, actions, qtable)

# Get the reward for that action

reward = 0

if random.random() < probabilities[action]:

reward = 5

episode_rewards += [reward]

times_selected[action] = times_selected[action] + 1

qtable.update(

state,

action,

(reward / times_selected[action])

- (qtable.get_q_value(state, action) / times_selected[action]),

)

rewards += [episode_rewards]

return rewards

\(\varepsilon\)-greedy strategy#

The \(\varepsilon\)-greedy strategy balances exploration and exploitation by setting the parameter \(\epsilon\) which controls how much the gambler explores. Each time she selects an action, the gambler uses this strategy:

With probability \(1-\varepsilon\), the gambler exploits the armed-bandit by picking the arm with the maximum Q-value (in the case of a tie between several actions, the tie is broken randomly);

With probability \(\varepsilon\), the gambler explores by picking a random arm, using a uniform probability to select her pick.

The \(\varepsilon\)-greedy strategy is implemented by the code below, using the random() function to pick a random number between \(0\) and \(1\).

import random

from multi_armed_bandit.multi_armed_bandit import MultiArmedBandit

class EpsilonGreedy(MultiArmedBandit):

def __init__(self, epsilon=0.1):

self.epsilon = epsilon

def reset(self):

pass

def select(self, state, actions, qfunction):

# Select a random action with epsilon probability

if random.random() < self.epsilon:

return random.choice(actions)

arg_max_q = qfunction.get_argmax_q(state, actions)

return arg_max_q

The following plot shows the reward for each step, averaged over 2000 episodes. Each episode is 1000 steps long. We evaluate different values of \(\epsilon\). The simulations illustrate the exploration-exploitation dilemna: High \(\epsilon\) have a lower reward in the long-run, but low \(\epsilon\) never converge to the opimal reward.

For our parametric example, choosing \(\epsilon\) between 0.05 and 0.1 is a good strategy. However, there is no universal value for the \(\epsilon\) parameter, its optimal value varies across applications.

Value Iteration#

Policy Evaluation#

Instead of jointly solving for the value function and optimal policy function, as done in previous chapters, we can instead start by exploiting an arbitrary policy and evaluate its value function.

We now provide an illustration of this approach for the optimal growth model.

#==============================================================================

# Optimal Growth: Evalution of Policy Function

#==============================================================================

import os

import numpy as np

from scipy.optimize import fminbound

def iterative_policy(w, pol, grid, β, u, f, Tw=None):

# === Apply linear interpolation to w === #

w_func = lambda x: np.interp(x, grid, w)

# == Initialize Tw if necessary == #

if Tw is None:

Tw = np.empty_like(w)

# == set Tw[i] = max_c { u(c) + β E w(f(y - c))} == #

for i, y in enumerate(grid):

Tw[i] = u(pol[i])+β * w_func(f(y - pol[i]))

return Tw

def solve_optgrowth_policy(initial_w, pol, grid, β, u, f, tol=1e-4, max_iter=500):

w = np.empty(len(grid))

# w = initial_w # Set initial condition

w[:] = initial_w # Set initial condition

error = tol + 1

i = 0

# == Create storage array for bellman_operator. Reduces memory

# allocation and speeds code up == #

Tw = np.empty(len(grid))

# Iterate to find solution

while error > tol and i < max_iter:

w_new = iterative_policy(w,

pol,

grid,

β,

u,

f,

Tw)

error = np.max(np.abs(w_new - w))

w[:] = w_new

i += 1

print("Iteration "+str(i)+'\n Error is '+str(error)+'\n') if i % 50 == 0 or error < tol else None

return [w]

class CES_OG:

"""

Constant elasticity of substitution optimal growth model so that

y = f(k) = k^α

The class holds parameters and true value and policy functions.

"""

def __init__(self, α=0.4, β=0.96, sigma=0.9):

self.α, self.β, self.sigma = α, β, sigma

def u(self, c):

" Utility "

return (c**(1-self.sigma)-1)/(1-self.sigma)

def f(self, k):

" Deterministic part of production function. "

return k**self.α

We instantiate the class CES_OG and define the grid.

# Creation of the model

ces = CES_OG()

# == Unpack parameters / functions for convenience == #

α, β, sigma = ces.α, ces.β, ces.sigma

### Setup of the grid

grid_max = 1 # Largest grid point

grid_size = 200 # Number of grid points

grid = np.linspace(1e-5, grid_max, grid_size)

Then we define the arbitrary policy to be evaluated.

# Policy function to be evaluated

policy = .5*grid

# Initial guess for the value function

guess_w = ces.u(policy)

Finally, we evaluate the value function associated to our arbitrary policy.

# Computation of the value function

solve = solve_optgrowth_policy(guess_w, policy, grid, β, u=ces.u,

f=ces.f, tol=1e-4, max_iter=500)

value_approx = solve[0]

Iteration 50

Error is 0.14170816828288224

Iteration 100

Error is 0.01840587788598924

Iteration 150

Error is 0.002390662054700954

Iteration 200

Error is 0.00031051303802343

Iteration 228

Error is 9.900892963088381e-05

#==============================================================================

# Plotting value function

#==============================================================================

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(9, 5))

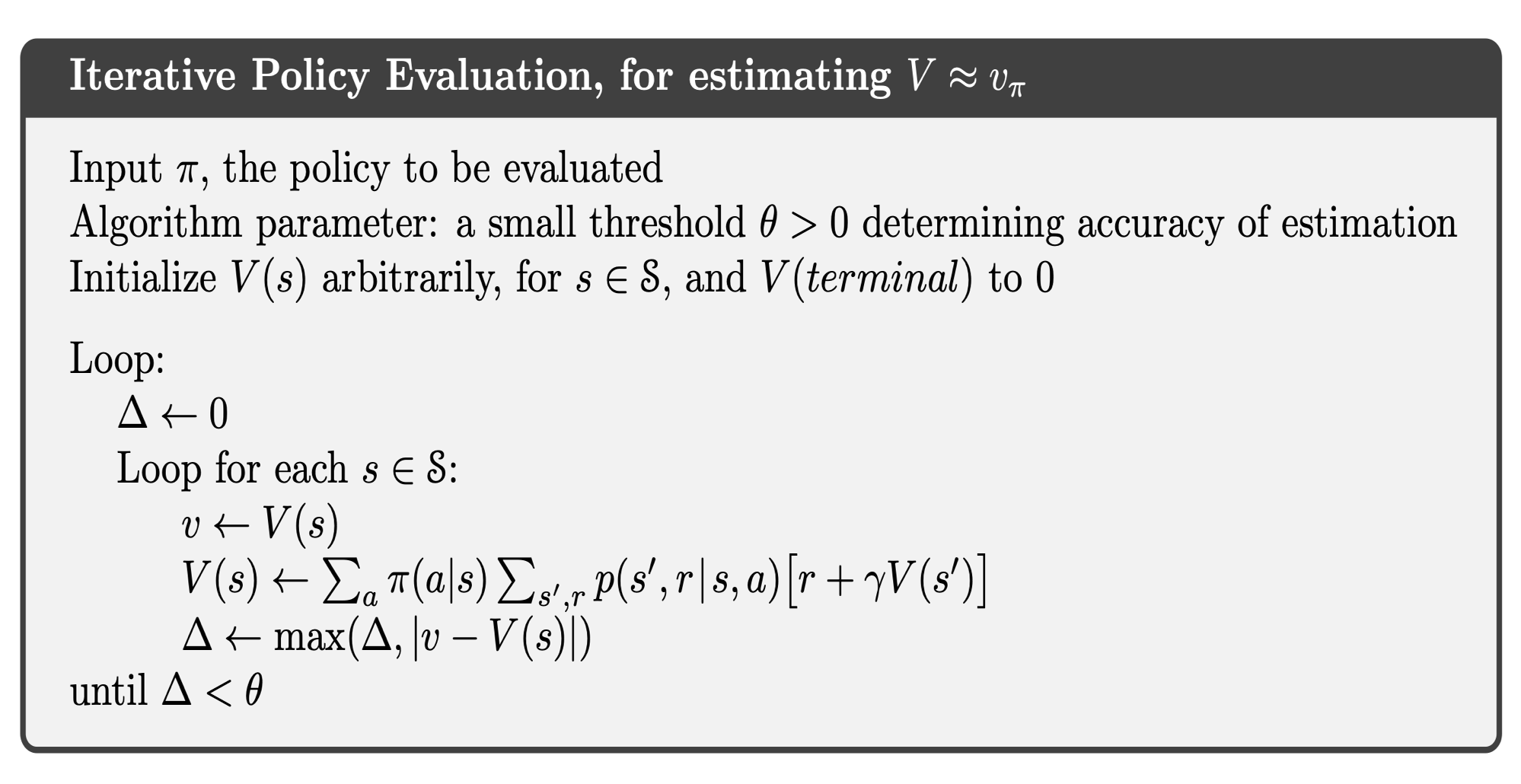

ax.plot(grid, value_approx, lw=2, alpha=0.6, label='approximate value function')

ax.plot(grid, guess_w, lw=2, alpha=0.6, label='guessed value function')

ax.set_xlabel('c')

ax.set_ylabel('v')

ax.legend(loc='lower right')

plt.show()

The figure above compares our initial guess with the approximated value function resulting from the arbitrary policy.

Policy Iteration#

We can combine policy evaluation with policy improvement to evaluate the value function generated by the optimal policy.

We now provide an illustration of this approach for the optimal growth model.

#==============================================================================

# Optimal Growth: Policy Iteration

#==============================================================================

def evaluation_policy(w, pol, grid, β, u, f):

# === Apply linear interpolation to w === #

w_func = lambda x: np.interp(x, grid, w)

Tw = np.empty_like(w)

# == set Tw[i] = max_c { u(c) + β E w(f(y - c))} == #

for i, y in enumerate(grid):

Tw[i] = u(pol[i])+β * w_func(f(y - pol[i]))

return Tw

def improve_policy(w, grid, β, u, f, Tw=None):

# === Apply linear interpolation to w === #

w_func = lambda x: np.interp(x, grid, w)

# == Initialize Tw if necessary == #

if Tw is None:

Tw = np.empty_like(w)

Tpolicy = np.empty_like(w)

# == set Tw[i] = max_c { u(c) + β E w(f(y - c))} == #

for i, y in enumerate(grid):

def objective(c, y=y):

return - u(c) - β * w_func(f(y - c))

c_star = fminbound(objective, 1e-10, y)

Tpolicy[i] = c_star

Tw[i] = - objective(c_star)

return Tw, Tpolicy

def solve_optgrowth_policy(initial_w, pol, grid, β, u, f, tol=1e-4, max_iter=500):

w = np.empty(len(grid))

w[:] = initial_w # Set initial condition

error = tol + 1

i = 0

# == Create storage array for bellman_operator. Reduces memory

# allocation and speeds code up == #

Tw = np.empty(len(grid))

# Iterate to find solution

while error > tol and i < max_iter:

w_new = evaluation_policy(w,

pol,

grid,

β,

u,

f)

error = np.max(np.abs(w_new - w))

w[:] = w_new

i += 1

return [w]

# Policy function to be evaluated

policy = .5*grid

# Initial guess for the value function

guess_w = ces.u(policy)

We provide below an example of how to compute the value function resulting from the conjectured policy, and then store in solve_improve the improved policy associated to the new value function.

# Computation of the initial value function

solve = solve_optgrowth_policy(guess_w, policy, grid, β, u=ces.u,

f=ces.f, tol=1e-4, max_iter=500)

value_approx = solve[0]

# Computation of the updated policy function

solve_improve = improve_policy(value_approx, grid, β, u=ces.u, f=ces.f)

Repeating the steps above iteratively until convergence allows us to approximate the true value function and optimal policy.

# Iterated procedure

tol=1e-4

error = tol + 1

i = 0

max_iter=500

w=np.empty(len(grid))

w[:] = guess_w

w_history = []

while error > tol and i < max_iter:

solve_eval = solve_optgrowth_policy(w, policy, grid, β, u=ces.u,

f=ces.f, tol=1e-4, max_iter=500)

w_approx = solve_eval[0]

solve_improve = improve_policy(w_approx, grid, β, u=ces.u, f=ces.f, Tw=None)

w_new = solve_improve[0]

policy_new=solve_improve[1]

error = np.max(np.abs(policy_new - policy))

policy[:] = policy_new

w[:] = w_new

w_history.append(w.copy()) # Append a copy of w to the list

i += 1

print("Iteration "+str(i)+'\n Error is '+str(error)+'\n')

value_final = w_new

Iteration 1

Error is 0.1310681176524393

Iteration 2

Error is 0.0061036722306999636

Iteration 3

Error is 0.0015584785903355325

Iteration 4

Error is 9.152334480444502e-05

#==============================================================================

# Plotting value functions

#==============================================================================

w_matrix = np.array(w_history) # Convert the list to a matrix

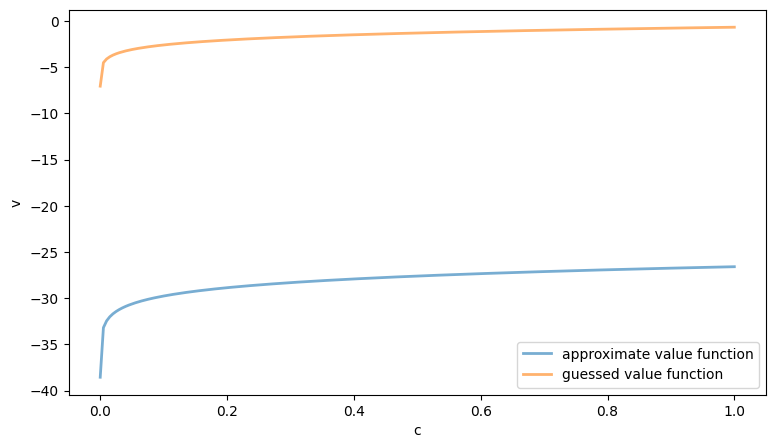

fig, ax = plt.subplots(figsize=(9, 5))

ax.set_ylim(min(value_final), max(value_final))

for i in range(w_matrix.shape[0]):

ax.plot(w_matrix[i], lw=2, alpha=0.6, label='Value Function at Iteration '+str(i+1))

ax.set_xlabel('c')

ax.set_ylabel('v')

ax.legend(loc='lower right')

plt.show()

The figure above shows the value functions at each iteration. Note that the total number of iterations is significantly smaller than in the nested procedure, where the value and policy functions are updated simultaneously.

Reinforcement Learning#

This repository provides code, exercises and solutions from

Each folder in the repository corresponds to one or more chapters of the above textbook and/or course. In addition to exercises and solution, each folder also contains a list of learning goals, a brief concept summary, and links to the relevant readings.

All code is written in Python 3 and uses RL environments from OpenAI Gym. Advanced techniques use Tensorflow for neural network implementations.